JHVEditorial photo/iStock via Getty Images

Growing recession concerns and rising interest rates have meant that any company with economic sensitivity, real or perceived, has been a hard sell. United Rentals (NYSE: URI), the nation’s largest equipment rental company, was is no exception to this trend. Shares fell sharply a third since their peak in 2021, although they have performed very well over the past decade as the company has consolidated smaller players, increased size and margins, while using free cash flow to buy back stock:

Looking for Alpha

It is important to note that this decline in share price was not caused by a deterioration in financial performance. In fact, after the second quarter, United Rentals raised its outlook for the year. The company will generate approximately $5.5 billion in EBITDA, which will drive approximately $2 billion in free cash flow in 2022.

United Rentals

The strong free cash flow comes even as the company invests heavily in expanding its rental equipment fleet, with rental purchases up about 11% to $1.35 billion. At the same time, its used equipment sales fell about 19% to $362 million. As a result, the book value of its rental equipment has increased nearly 5% year-to-date to $11.03 billion. The company is able to invest in expanding its fleet while generating significant free cash flow. Amid its outlook, URI trades at just 9.5 times that free cash flow, an attractive valuation.

It is important to note that URI does not just grow its fleet for fun. Indeed, if the company could not rent additional equipment, as shareholders, we would not want them to buy more. That’s why I like to look at fleet productivity, which combines changes in rental rates and utilizations to determine how much incremental revenue the company gets from each piece of equipment. That figure is up 11.3% in the second quarter, meaning the company is able to charge more for its equipment and rent it out more frequently. In this environment where demand exceeds supply, rental fleet expansion can be highly accretive to shareholders.

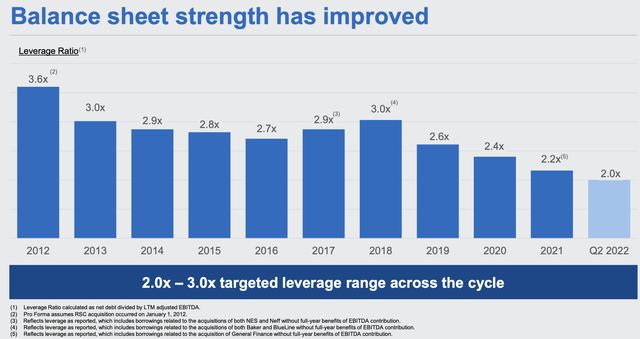

As United Rentals grew, it also strengthened the strength of its balance sheet. The company is now targeting a debt to EBITDA ratio of 2 to 3x, compared to 2.5 to 3.5x several years ago. Right now, the firm’s leverage is just at the bottom of the target at 2.0x. Businesses with more leverage are at risk when interest rates rise if they have to refinance maturities at higher rates, which increases interest expense and reduces free cash flow. URI’s low leverage positions it well for a period of rising rates. Indeed, a return to the midpoint of its debt target would mean additional debt of $2.7 billion. This gives the company significant ability to make an acquisition if an opportunity arises.

United Rentals

Because the company does not need to focus on paying down debt, it can instead focus on buying back stock. In the first half of this year, the company repurchased $762 million in stock and expects to have reached its 2022 target of $1 billion by the end of the third quarter. These stock buybacks add up over time. In 2015, URI had 95.2 million shares outstanding. Today, the company has 71.2 million outstanding, a reduction of 25.2%. So during this period, while net income increased 200% to $1.75 billion, net earnings per share increased 294%. The combination of underlying business growth and declining share count provides explosive growth for shareholders, generating very good returns over time.

With the company’s strong free cash flow generation, it is well positioned to reduce its share count by 5-10% per year over the next 3 years, which will help further accelerate EPS growth in beyond the $25 or so that I expect to earn this year. Importantly, I believe the company will be able to maintain strong free cash flow results over this period.

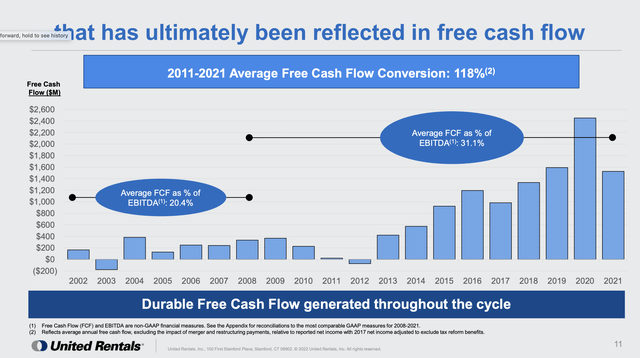

While equipment usage is thought to be highly cyclical, United Rentals actually has counter-cyclical free cash flow. The graph below shows two things. First, how much incremental free cash flow has the company generated in recent years by consolidating the equipment rental business, which has led to greater scale and higher margins. Second, free cash flow actually increased in 2008 and 2020, the two years we enter recession.

United Rentals

There are two reasons for this. First, during times of economic uncertainty, businesses are more likely to lease equipment than to purchase their own. So while overall equipment usage may drop in a downturn, the URI gets a bigger slice of that pie. Second, the URI has considerable flexibility over its cap-ex. As usage decreases, she can extend the age of her fleet. Rather than selling equipment after three years, he can keep a quarter or a fifth. This significantly reduces capital expenditures, which increases free cash flow. Then, as the economy rebounds (as in 2011-2012), it spends to expand its fleet, reducing free cash flow this year but creating the foundation for higher cash flow in years to come. .

So even if you’re worried about an economic downturn, by reducing fleet purchases, URI could generate more cash and actually be able to increase stock buyback, which if done when the stock market is lower (as it may be in a recession) be even more accretive to earnings per share. However, I suspect that demand for URI equipment may prove more resilient than some fears. First, only 4% of its activity is related to residential construction, and it’s mostly multi-family, so as higher rates slow single-family construction, there’s very little impact.

Additionally, last year Congress passed a new infrastructure bill that continues to gain momentum as major projects take time to clear. This year, the CHIPS Act was passed to spur the construction of semiconductor factories, and state governments have strong finances. Increased government construction spending will drive demand for equipment, and URI derives nearly half of its revenue from non-residential construction. The demand here may actually increase accordingly.

The other half of its activity is related to the use of industrial equipment, the energy and chemical sectors being particularly important. Oil and gas investment has increased due to rising prices, and with Europe moving away from Russian energy, there is room for U.S. energy infrastructure spending to rise for respond to this request. Additionally, the recently passed Inflation Reduction Act specifically targets increased energy infrastructure spending. These sources of demand provide grounds for optimism even as the rest of the economy slows.

Of course, no investment is without risk. If business investment and construction activity were to slump, even if rental equipment gained market share, demand would likely plummet and result in lower fleet productivity. While URI can compensate for this to some degree by aging its fleet, if demand were to drop more than 15%, free cash flow would likely decline, although given the tailwinds I’ve listed, I views this difficult scenario as unlikely.

URI is also better positioned than its peers during downturns. The equipment rental market is very diffuse, with URI having a market share of over 15%, and 71% of the market is controlled by companies with less than 3% market share. With smaller scale, lower margins and less balance sheet flexibility than URI, they would likely suffer more. Indeed, the latest downturn has provided URI with the opportunity to consolidate smaller players, add scale and increase margins. So while the downturn will create short-term headwinds, there would potentially be long-term gains.

Because URI is acquisitive, having made over 300 acquisitions large and small, there is always the risk management of making an acquisition too expensive or expanding its fleet at the wrong time. Management missteps are a risk with any investment, but URI has proven to be a strong acquirer, as evidenced by its long-term free cash flow growth, share price performance and growth. margin expansion. He has also shown excellent discipline in recent years by reducing leverage rather than buying companies at the top of the market. Now, he has the ability to make deals if opportunities arise. It’s a risk I think investors should feel comfortable taking.

Overall, URI is a proven free cash flow machine that aggressively buys back stocks, has the business mix to weather an economic downturn, and can really increase free cash flow during downturns by aging its fleet. . However, given its mix of activities, demand should remain strong, which will help to further increase rental rates.

I think the stock should trade at a free cash flow yield of around 8%, given its continued strong repurchase ability, which at a rate of $2 billion equates to a stock price of stock around $350, a multiple of 14x P/E, offering almost 30% upside from current levels. I would recommend accumulating stocks here and letting the power of URI’s redemptions and cash generation provide strong returns over time.